Baker Brothers Renewed Their Acadia Exit Infrastructure

Baker Bros filed Schedule 13D Amendment 17 on Acadia showing a renegotiated registration rights agreement allowing block trades. We pulled 14 years of Baker's 13D filing history to see what this could mean.

Baker Brothers1 filed Amendment 17 on their Acadia Pharmaceuticals Schedule 13D on February 26, 2026. The filings didn’t reflect a change in Baker’s ~25% stake (43 million shares) in the company, but it did describe a renewed and amended agreement that caught our eye.

Baker Brothers Renews Registration Right Agreement with Acadia Pharmaceuticals #

The new Baker Brothers filing indicates that Baker and Acadia entered into a new Registration Rights Agreement (RRA) stipulating:

- Acadia must file a resale S-3 shelf upon Baker’s request

- Baker gets one underwritten public offering per calendar year, three total

- Baker also gets two underwritten offerings or block trades per 12-month period

- Rights last 10 years, covering all equity and certain debt securities

Baker and Acadia had a RRA from January 2016 that was tied to a follow-on offering. That agreement expired in January of this year. This newly disclosed RRA is “standalone” in that it is not tied to a new share offering or private placement and it explicitly adds block trade rights (two per 12-month period) as well as extending coverage to debt securities.

Block Trading Provides Institutional Liquidity

Block trading rights are important liquidity mechanisms for firms like Baker that own huge portions of companies (~25% in this case), since SEC Rule 144 limits open sales to about 1% of outstanding shares per quarter, not to mention the price impact of dumping millions of shares on the open market. Block trading allows Baker to sell large blocks of shares to institutional buyers at smaller discounts.

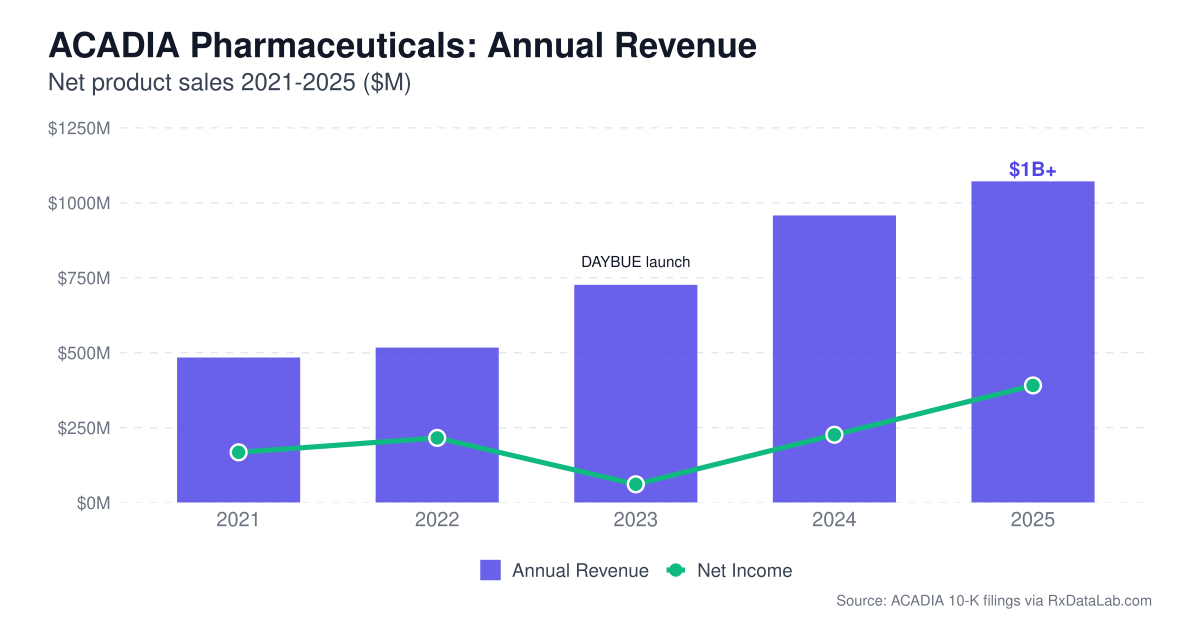

Acadia had a strong 2025, with their latest 10-K showing revenue crossing $1B ($1.07B, up from $958M in 2024) and net income nearly doubling to $391M, driven by DAYBUE, their Rett Syndrome Drug. Acadia’s 2026 guidance projects continued growth. However, they also experienced a setback in Europe, with the EMA rejecting marketing authorization for DAYBUE due to a small effect size “unlikely to be clinically meaningful” and various other issues. Acadia has requested re-examination with the EMA.

ACADIA Pharmaceuticals: Annual Revenue

Source: ACADIA 10-K filings via RxDataLab.com

Given Acadia’s recent performance, we wondered whether this RRA was a routine amendment and renewal or a sign of Baker prepping an imminent exit.

14 Years of Baker Brothers Activist Holdings #

RxDataLab aggregates regulatory, trial, and market data for the biotech industry. To better understand this move in the context of Baker’s historical behavior, we pulled all of Baker Brothers’s 13D filings for the past 14 years and analyzed the disclosure text. Schedule 13D filings are required for institutional owners who control more than 5% of a company with the intent to influence management or direction. You can read more about Schedule 13 filings in our post about understanding beneficial ownership in biotech. We found ~203 activist filings across 38 companies since 2012 and plotted them on the timeline below, colored by outcome and with RRA’s indicated with diamonds.

Baker Bros 13D Holding Periods, 2012–2026

Diamonds mark when Baker obtained registration rights.

One thing that stands out is that based on our records, Acadia is Baker’s longest held activist position at ~13 years2. Baker was a 13D filer for roughly 10 years with Seattle Genomics before the Pfizer acquisition.

When analyzing the Item 6 text of the filings, we noted that most RRA language in Baker’s filings are routine deal terms, such as the 2024 wave (Bicycle Therapeutics, Kymera, HOOKIPA, Entrada, Kala Bio) which all came attached to new Securities Purchase Agreements. Baker puts money in and the company provides registration rights as a standard condition.

We found just two standalone RRA renewals not tied to any new investment: Acadia (February 24, 2026) and Incyte (February 6, 2026). Both were entered very recently, just a few weeks apart.

What This Could Mean #

A renewed standalone RRA could mean a few things.

Baker is preparing to exit. A block trade is exactly the mechanism you’d use to sell 43 million shares to institutional buyers in one transaction. Baker has held Acadia for 13 years. At some point, even a long-duration fund needs liquidity. The new RRA is how they do it cleanly.

A sale of Acadia is being prepared. If a CNS or rare disease acquirer is circling Acadia, Baker’s participation as a 25% holder with a board seat is non-negotiable. Freshly-registered shares are clean, deal mechanics are already in place, Baker doesn’t need to negotiate anything mid-transaction.

Nothing. Of course, this could simply be a routine renewal of a commercial stage company and no imminent exit or sale is coming. Under the terms of the agreement, Baker could hold Acadia for another decade before taking any action.

Of Baker’s three confirmed large exits, Seattle Genetics had an offering-linked RRA from September 2015, seven years before Pfizer acquired them in 2022.

What was interesting about the RRA was that it was a standalone renewal not tied to a new investment, and that it included block trading rights. After looking at the data, there isn’t much to say definitely about what Baker plans to do based on previous behavior. One thing is clear: Baker is now unlikely to passively bleed down their position. When Baker exits quietly, they simply stop filing 13D’s once they drop below 5% - no infrastructure needed, as they did with Mirati over six years. If that were the plan here, they likely wouldn’t be signing new legal agreements with Acadia.

In our opinion, this renewal is preparation for something that requires a clean, fast exit.

What to Watch #

- An Acadia S-3 shelf registration: Acadia filing a resale shelf for Baker’s shares is the first activated step. No immediate market action, but it means the clock has started.

- A block trade announcement: large registered secondary, executed in a single session with institutional buyers, announced same-day.

- Baker’s next 13D/A: any change in Item 4 language or a reduction in position.

Baker Brothers, Acadia, and every 13D/G filer across 500+ biotech companies are tracked in real time on BioHedge, RxDataLab’s free institutional ownership tracker. When Baker’s next filing drops, it shows up there first. See more about the full RxDataLab Platform.

Data: Baker Bros. Advisors LP (CIK 1263508) Schedule 13D filings, EDGAR. Analysis covers 203 filings across 38 companies, 2012–2026.

See Baker Brothers CIK 1263508 ↩︎

Note this is the longest 13D activist holding, that does not mean it is Baker’s longest held position. We did not perform longest held position for this piece. ↩︎

RxDataLab Research Notes

Primary-source analysis of biotech companies: clinical trials, SEC filings, and hedge fund positioning. Get notified when we publish. No fixed schedule, no filler.