SEC Ownership Filings in Biotech and What We Can Learn From Them

How to read SEC beneficial ownership and insider reporting filings such as Schedule 13D, 13G, Form 13F, and Form 4 and what they reveal when you layer them together for biotech companies.

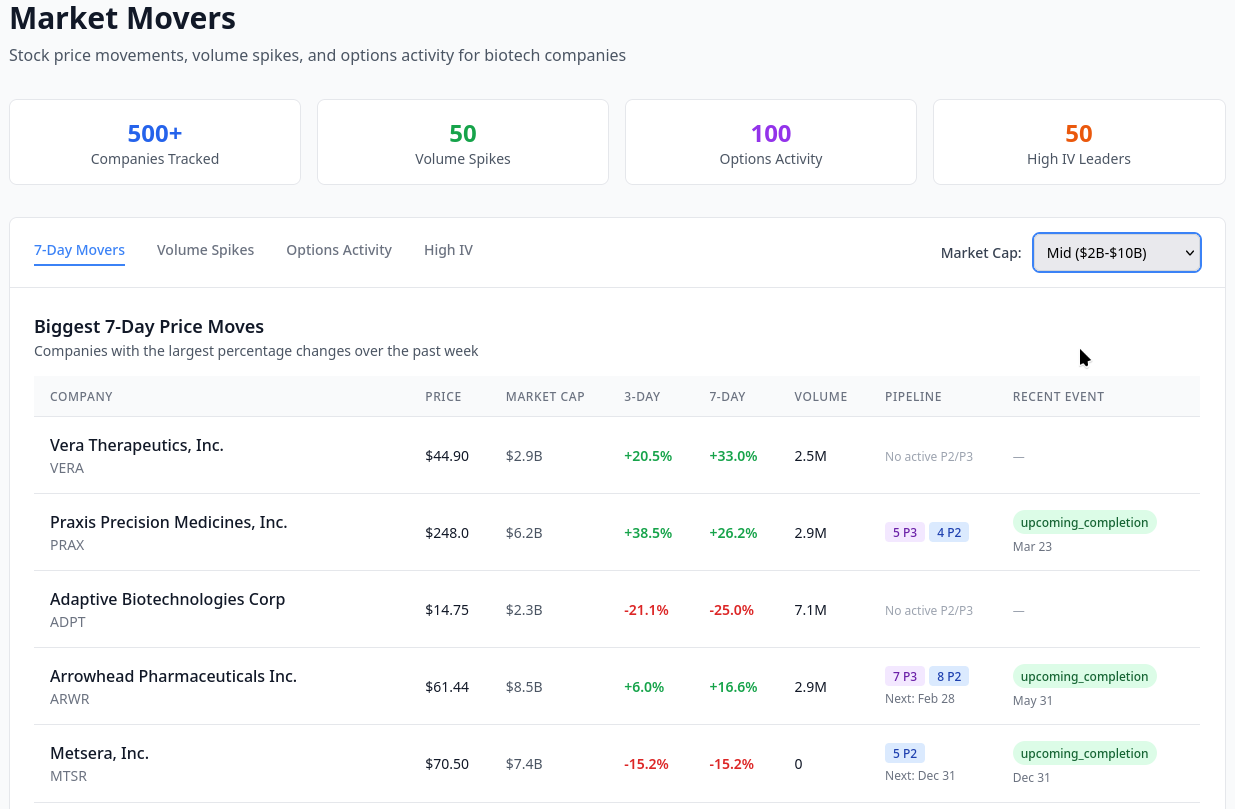

Track 13D, 13G, and 13F filings alongside insider transactions, clinical trial pipelines and regulatory filings for 500+ public biotech companies on RxDataLab.

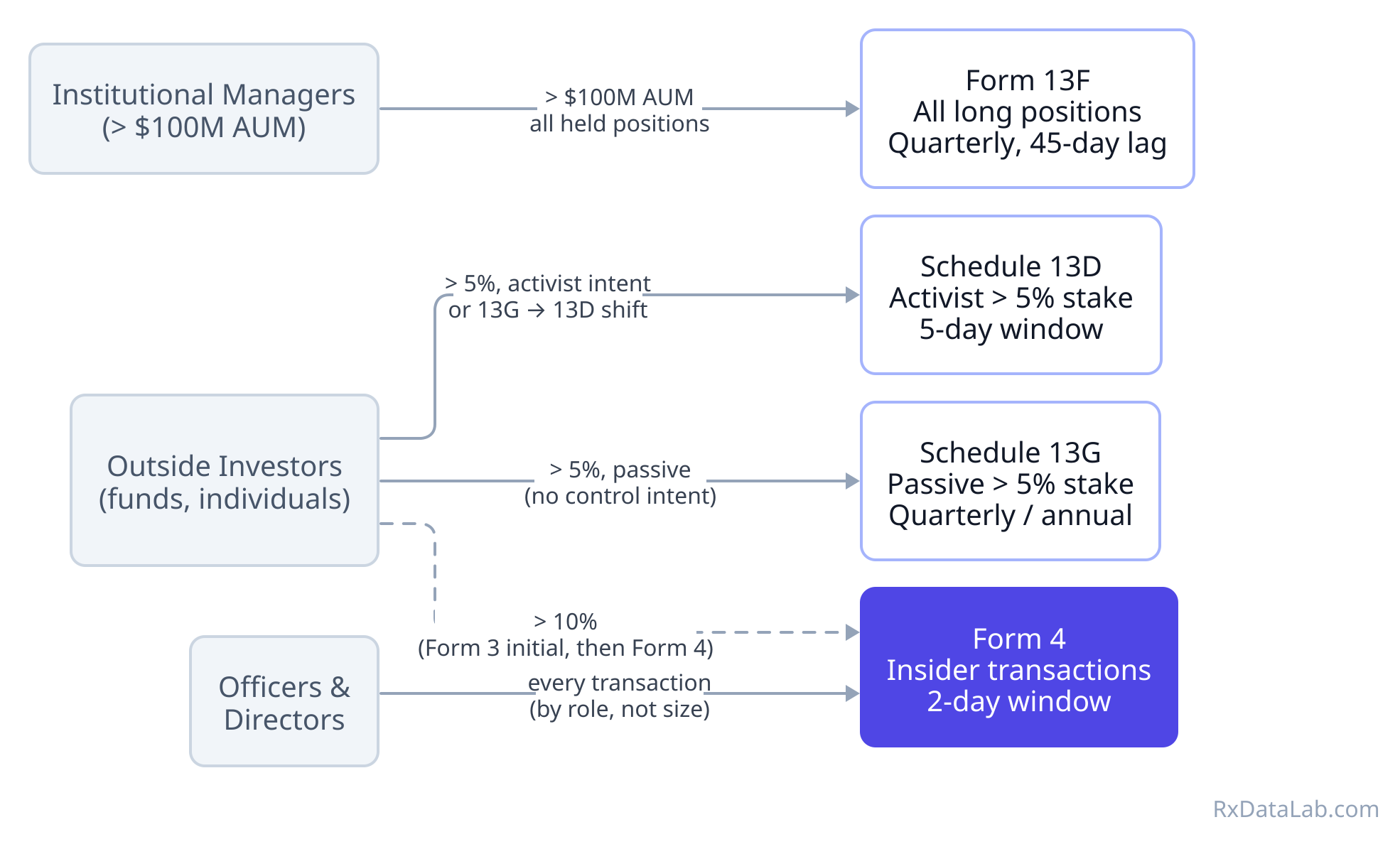

Monitoring insider transactions and institutional ownership at a high level requires understanding four disclosures: Schedule 13 (13D, 13G), Section 13F, and Form 4. Each tells you something different about how company insiders or high-percentage owners are behaving, and if you’re careful, it can give you clues about what they will do next.

Who Files What #

Filing requirements differ based on who you are as well as how much you own. There are three distinct populations:

Company insiders, officers, and directors file Form 4 due to their role, regardless of position size. This means a CEO who owns 0.2% of the company has to report every open-market purchase or sale within 2 business days. Insider status is defined by your relationship to the company.

Outside investors need to file disclosures via Schedule 13 when they accumulate over 5% of the company. Below that level, they are invisible. Above 5%, how they report will depend on their intent with their ownership. For example, if they plan to influence the board or company direction, they will file Schedule 13D. If they simply plan to watch from the sidelines, then Schedule 13G. 13D and G have different filing frequencies/deadlines that we will cover below. Outside investors crossing 10% must first file Form 3 (an initial statement of beneficial ownership), then report all subsequent position changes on Form 4 (covered below).

Institutional investment managers or anyone with more than $100 million in assets under management (AUM) file Form 13F quarterly. 13F lists every long equity position they hold, regardless of size in any individual company. 13F is typically what people are analyzing quarterly when you see articles about hedge fund holdings. This report is useful because a fund managing $500M files 13F on every position, including 1% stakes that would never trigger a 13D or 13G. 13F is the broad institutional picture, while 13D and 13G are concentrated-holder pictures.

Schedule 13D Activist Disclosure #

As described above, Schedule 13D is filed when any person acquires beneficial ownership of more than 5% of a registered equity class with intent to influence or change control of the company1. As of February 2024, the filing deadline is 5 calendar days after crossing the threshold tightened from 10 days.2 Amendments are due within 2 business days of any material change, including a position change of more than 1%.

In addition to the equity stake, 13D has many standard listing items. Most of it is boilerplate, but two items are worth noting when reading 13D:

Item 4: Purpose of Transaction

This is the narrative disclosure of why the filer owns the position and what they intend to do. At minimum it says something like “the reporting persons acquired the securities for investment purposes and may engage with management.” It can also include board letters, public statements of activist intent, demands for strategic review, or explicit statements that the filer is exploring a sale.

For example, this is an excerpt of an Item 4 for a 13D filed by RA Capital Management for Sionna Therapeutics Inc.

…consistent with their investment purpose, the Reporting Persons may engage in communications with persons associated with the Issuer, including stockholders of the Issuer, officers of the Issuer, members of the board of directors of the Issuer, and/or or other third parties, to discuss matters regarding the Issuer, including but not limited to its operations, strategic direction, governance or capitalization, and potential business combinations or dispositions involving the Issuer or certain of its businesses…"

RA Cap has a board seat at Sionna and owned roughly a quarter of the company in February 2025 when this was filed.

Item 6: Contracts, Arrangements, Understandings

Item 6 lists details about side agreements such as registration rights agreements, lock-up provisions, co-investment rights, board nomination rights.

For example, Baker Brothers Advisors LP, which owns ~25% of Acadia Pharmaceuticals, filed a 13D amendment in February 2026 disclosing a registration rights agreement with Acadia. The agreement obligates Acadia to file a shelf registration statement on demand, which effectively makes Baker Bros’ stake freely tradeable and enabling structured exits. Without registration, a holder of that size faces Rule 144 volume limits that would make selling a meaningful portion of their position extremely slow.

“…the Funds have the right to (i) one underwritten public offering per calendar year, but no more than three underwritten public offerings in total, and (ii) no more than two underwritten public offerings or block trades in any twelve-month period, to effect the sale or distribution of Registrable Securities…”

The agreement gives Baker Bros up to one underwritten public offering per year (three total) and two block trades or offerings in any twelve-month period. A more detailed article about this Baker Bros filing is in progress.

The rate of 13D amendments can also indicate how active the fund is, as any material change in their position or posture requires a new filing.

Relevant Laws and Regulations

Schedule 13G Passive Ownership #

Schedule 13G covers the same 5% threshold but for investors holding the position without intent to influence or control the company.3 These disclosures are shorter and have less stringent amendment deadlines, but the deadlines vary by filer category.

For example, in 2024 deadlines tightened for Qualified Investment Institutions (QIIs), which now must file within 45 days of quarter-end after crossing 5%, where they previously only had to file 45 days after calendar year-end. Passive investors file within 5 calendar days of crossing 5%. This is why you’ll see a large volume of 13G disclosures on BioHedge, our biotech hedge fund filing tracker around a month after quarter end.

With 13G filings, it is worth watching accumulation and disposal patterns, and especially passive-to-active (13G to 13D) transitions. So even though these filings don’t have the informative Item 4 and 6 that 13D mandates, you can still use these filings to monitor holdings and activity.

Relevant Laws and Regulations

Institutional Ownership Snapshots on Form 13F #

Any institutional investment manager with more than $100 million in AUM must file a quarterly disclosure on every Section 13(f) security they hold4. The SEC publishes a quarterly list of 13(f) securities, which are primarily U.S.-listed equities and options5. The form is due within 45 days of quarter-end.6

13F is an information-rich document, and you will often see sensational news articles and analysis of company holdings after these forms are released. But it is important to recognize that 13F is a snapshot, not a transaction log. A fund could acquire and dispose of multiple positions during a month and it would never appear on their 13F unless they held it on the last trading day of the quarter.

13F lists Section 13(f) positions as of the last trading day of the quarter, and includes issuer name, CUSIP7, market value, share count, and voting authority.

13F Caveats

There are a few caveats when interpreting 13F filings that are often missed. First, it is important to realize it is a snapshot of Section 13(f) positions held as of the end of a given quarter. That means a firm could enter and exit positions mid-quarter, and as long as they didn’t hold the positions on the filing deadline, you’d never see them. Also, by the time a 13F is public, the data is already 45 days old. By the time the next quarter’s 13F is due, the prior quarter’s filing can be 135 days stale. Managers can also request confidential treatment for positions still being established, delaying disclosure further.8

Short positions aren’t reported. Options and other derivatives aren’t required (though some managers voluntarily include them). Non-U.S. listed securities, private company holdings, and convertible notes aren’t covered. For biotech specifically, many crossover funds have significant convertible note positions and private company holdings that won’t appear in 13F data.

Given those caveats, 13F is still a useful tool to see which funds are building or reducing long positions over time, and can reveal holdings that might be below the Schedule 13 filing requirements but still significant.

Relevant Laws and Regulations

Form 4 Insider Transactions #

Form 4 is how company officers, directors, and >10% owners report changes to their beneficial ownership. The 2-business-day filing window (established by Sarbanes-Oxley in 2002, tightened from 10 days) makes this the fastest-updating of the four streams.9

Each Form 4 shows a transaction date, a single-letter transaction code, share count, price, and post-transaction ownership total. Transaction codes include:

| Code | Meaning |

|---|---|

P | Open market purchase |

S | Open market sale |

A | Grant, award, or acquisition from the company |

M | Option exercise |

F | Share withheld for tax or exercise cost |

G | Gift |

The P and S codes are important if you’re looking for insider signals. An open-market purchase or sale means an insider chose to deploy their own capital at market prices. A transactions are compensation, such as a stock grant or award from the company.

The acquired_disposed field (A for acquired, D for disposed) is the authoritative direction indicator and must be read alongside the transaction code. A tax withholding (F) is technically a “disposal” even though it’s just the company taking back shares to cover taxes. It doesn’t mean the insider sold.

10b5-1 plans

10b5-1 plans are pre-arranged trading schedules an insider sets up in advance. They function as affirmative defenses against insider trading allegations: if trading decisions were established on a fixed schedule months earlier, they are less likely to reflect material non-public information available at execution. Sales under a 10b5-1 are flagged on the Form 4, but the plan terms (price thresholds, date triggers, quantities) are not filed with the SEC and are not public.10 This makes them less informative as transaction signals, since the timing and size are allegedly predetermined. The SEC substantially tightened Rule 10b5-1 in December 2022, adding mandatory cooling-off periods and restrictions on single-trade plans after years of documented abuse.11

Biotech is a structurally unusual case for these plans. In most industries, the gap between when management knows material information and when it becomes public is relatively short. In clinical-stage biotech, trial data is generated and analyzed many months before public disclosure, so the company has visibility into emerging results long before a press release goes out. A plan adopted six months before a readout may be chronologically distanced from the announcement while still potentially being adopted in a period when internal data trends were becoming clear. We looked at this pattern in Wave Life Sciences, where eight executive plans adopted months apart all executed on the same day as a positive interim trial announcement. Easily explained by 10b5-1 plans with sales triggered by a price spike, but still a coincidence that illustrates the structural problem with these plans in biotech.

Relevant Laws and Regulations

Reading Them Together #

While each form is useful on its own, combining them (while understanding caveats and limitations) can give you a more complete picture of what investors and insiders are thinking, since each one answers a different question:

- 13F tells you which institutions are broadly exposed and roughly how much

- 13G tells you which of those is a concentrated passive holder above 5%

- 13D tells you which large holder has declared activist intent — and through Item 4 and Item 6, what they’re actually doing or planning

- Form 4 tells you what the people inside the company are doing with their own money, and at what speed

The overlap zone worth watching: when a fund crosses 10%, they’re now both on a 13D or 13G and required to file Form 4 on transactions. You’ll see the same fund in both streams. These positions are actually very common in biotech, as hedge funds hold huge stakes in companies that they might have taken from venture funding through IPOs.

At RxDataLab, we parse all four form types for 500+ public biotech companies using our own Go-based parser, linked on the backend to company CIK and trial registry records. The BioHedge dashboard tracks 13D and 13G filings in near-real time across biotech-focused institutional funds. Strategic Signals surfaces 8-K-derived business development events (licensing deals, strategic reviews, and financing activity). We also parse quarterly 13F holdings and track insider activity via Form 4 with transaction type classification for every public US company.

Primary References

- Securities Exchange Act of 1934, Section 13

- Securities Exchange Act of 1934, Section 16

- 17 CFR Part 240 — General Rules and Regulations, Securities Exchange Act

- SEC Final Rule on 13D/13G amendments, Release No. 34-98704 (2023)

- SEC Rule 10b5-1 amendments, Release No. 34-96492 (2022)

- SEC 13F FAQ

17 CFR 240.13d-1(a). ↩︎

SEC Final Rule, Release No. 34-98704, adopted October 2023, effective February 5, 2024. ↩︎

17 CFR 240.13d-1(b) and (c). ↩︎

The SEC maintains lists of 13F securities updated quarterly ↩︎

17 CFR 240.13f-1(a). The $100M threshold has not changed since 1978. The SEC proposed raising it to $3.5B in 2020, which would have eliminated most current filers. The proposal was withdrawn in 2023. ↩︎

17 CFR 240.13f-1(a)(1). ↩︎

Committee on Uniform Securities Identification Procedures. CUSIP is a 9 character ID that uniquely identifies a company or issuer and type of financial instrument. For more, see: https://www.investor.gov/introduction-investing/investing-basics/glossary/cusip-number ↩︎

17 CFR 240.13f-1(b). Confidential positions are eventually disclosed but with delay. ↩︎

17 CFR 240.16a-3(g). ↩︎

Rule 10b5-1 is codified at 17 CFR 240.10b5-1. ↩︎

SEC Release No. 34-96492, December 2022, effective February 27, 2023. ↩︎

RxDataLab Research Notes

Primary-source analysis of biotech companies: clinical trials, SEC filings, and hedge fund positioning. Get notified when we publish. No fixed schedule, no filler.